新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

ACCA F8考试:USING THE WORK OF INTERNAL AUDITORS(二)

Step 2A: Evaluation of the existence and significance of threats to objectivity of the internal auditors

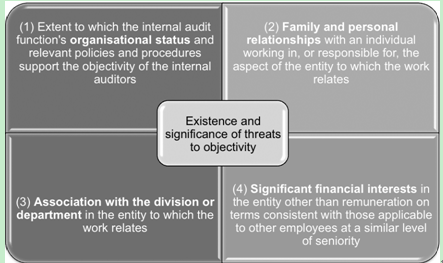

This is considered as an important element in the external auditor’s judgment as to whether internal auditors can provide direct assistance. Objectivity is regarded as the ability to perform the tasks without allowing bias, conflict of interest or undue influence of others to override professional judgment. The following factors are relevant to the external auditor’s evaluation of objectivity:

It should be noted that the main purpose here is to evaluate threats to objectivity. Take the first factor as an example – if evidence shows that the internal audit function’s organisational status supports the objectivity of the internal auditors, the external auditor will feel more comfortable using direct assistance from the internal auditors. The following situations are likely to support the objectivity of the internal auditors:

The internal audit function reports to those charged with governance (eg the audit committee) rather than solely to management (eg the chief finance officer)

The internal audit function does not have managerial or operational duties that are outside of the internal audit function

The internal auditors are members of relevant professional bodies obligating their compliance with relevant professional standards relating to objectivity.

Step 2B: Evaluation of the level of competence of the internal auditors

Competence of the internal audit function is likely to be deemed satisfactory where it can be evidenced that the function as a whole operates at the level required to (i) enable assigned tasks to be performed diligently and (ii) in accordance with applicable professional standards. To make such evaluation, the external auditor can take into consideration the following factors:

Whether there are established policies for hiring, training and assigning internal auditors to internal audit engagements

Whether the internal auditors have adequate technical training and proficiency in auditing (eg with relevant professional designation and experience)

Whether the internal auditors possess the required knowledge relating to the entity’s financial reporting and the applicable financial reporting framework

Whether the internal audit function possesses the necessary skills (for example, industry-specific knowledge) to perform work related to the entity’s financial statements.

Points to note in the evaluation

The above evaluation regarding the internal auditors’ objectivity and competence should not be new to candidates as it forms the basis for any assessment by the external auditor when determining if reliance can be placed on the work of internal auditors and as such the requirement for these evaluations has been present in previous versions of ISA 610. The external auditor should bear in mind that the assessment of competence and objectivity are of equal importance, and should be assessed individually and in aggregate. For example if the internal auditors are deemed appropriately competent but the external auditor identifies significant threats to objectivity it is unlikely that the external auditor will be able to use the internal auditors to provide direct assistance and vice versa.

Copyright © 2000 - www.chinaacc.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

新用户扫码下载

新用户扫码下载