新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

This article provides a broad overview of microeconomics. It is intended to introduce key topics to those who have not studied microeconomics, and to offer a revision to those who have done so

WHAT IS MICROECONOMICS?

Microeconomics is the branch of economics that considers the behaviour of decision takers within the economy, such as individuals, households and firms. The word ‘firm’ is used generically to refer to all types of business. Microeconomics contrasts with the study of macroeconomics, which considers the economy as a whole.

SCARCITY, CHOICE AND OPPORTUNITY COST

The platform on which microeconomic thought is built lies at the very heart of economic thinking – namely, how decision takers choose between scarce resources that have alternative uses. Consumers demand goods and services and producers offer these for sale, but nobody can take everything they want from the economic system. Choices have to be made, and for every choice made something is forgone. An individual may choose to buy a car, but in doing so may have to give up a holiday which they might have used the money for, if they had not chosen to buy the car. In this example, the holiday is the opportunity cost of the car. Just as individuals and households make opportunity cost decisions about what they consume, so too do firms take decisions about what to produce, and in doing so preclude themselves from producing alternative goods and services.

Producers also have to decide how much to produce and for whom. A simple answer to the first question might be: ‘As much as possible of course, using all the resources we can’. However, classical economists teach us that if we combine all of the factors of production – land, labour, capital and the entrepreneur – in different ways, we can get some surprising results. One of the most famous of these is confirmed by the law of diminishing returns. This law states that if we keep on adding variable factors of production (such as labour) to fixed factors (such as land), we will get proportionally less output from each additional unit of factor added until, eventually, overall output will start to decrease with each additional unit of factor added.

THE PRICE MECHANISM

Much of the study of microeconomics is devoted to analysis of how prices are determined in markets. A market is any system through which producers and consumers come together. In early subsistence economies, markets were usually physical locations where people would come together to trade. In more complex

economic systems, markets do not depend on humans actually meeting one another, so many markets today arise when producers and consumers come together less directly, such as by post and on the internet.

Producers and consumers generate forces that we call supply and demand respectively, and it is their interaction within the market that creates the price mechanism. This mechanism was once famously described as the ‘invisible hand’ that guides the actions of producers and consumers.

Markets are essential to produce the goods and services required for everyday life. Even if an individual can produce all the food needed to survive, that person will still need clothes, shelter and other necessities. Therefore, from very early times, communities learned that they would benefit from exchange. The crudest form of exchange was barter, but the evolution of money as a medium of exchange and unit of account accelerated the development of the process.

But how would people know what they could charge, or what they should pay, for goods and services? Before any formal thought was given to this, traders soon discovered that if they fixed their prices too low they would soon run out of inventory, while if they set their prices too high they would not sell what they had produced. In physical markets there would often be perfect knowledge, as traders would be able to check the prices of those who had similar goods and services to trade, simply by walking around the stalls. Once markets became more remote, less perfect knowledge of prices was inevitable and the process became less certain.

Alfred Marshall, whose Principles of Economics was published in 1890, drew heavily on the writings of Jevons and Mill. However, much of what you read today about supply and demand, elasticity, revenues and costs and marginal utility are based on Marshall’s thoughts. Marshall provided a base upon which formal analysis of supply and demand, and consequently the determination of prices in markets, could be built.

DEMAND

Demand is created by the needs of consumers, and the nature of demand owes much to the underpinning worth that consumers perceive the good or service to have. We all need necessities, such as basic foodstuffs, but other products may be highly sought after by some and regarded as worthless by others.

The level of demand for a good or service is determined by several factors, including:

· the price of the good or service

· prices of other goods and services, especially substitutes and complements

· income

· tastes and preferences

· expectations.

In orthodox economic analysis, these determinants are analysed by testing the

quantity demanded against one of these variables, holding all others to be constant (or ceteris paribus).

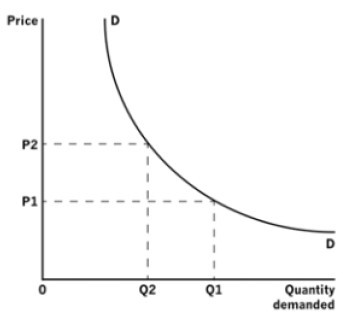

The most common way of analysing demand is to consider the relationship between quantity demanded and price. Assuming that people behave rationally, and that other determinants of demand are constant, the quantity demanded has an inverse relationship with price. Therefore, if price increases, the quantity demanded falls, and vice versa. Figure 1 portrays the conventional demand curve.

Figure 1: Demand curve

For any change in price, there is an inverse change in quantity demanded. The price increase from OP1 to OP1 results in a reduction in quantity demanded from OQ1 to OQ2.

A change in price will cause a movement along the curve. When the price increases, the quantity demanded will reduce. This happens with most types of goods, with some bizarre exceptions. Demand for what are known as ‘Giffen goods’ actually rises with an increase in the price for such goods. For example, when the price of rice increases in some regions of China, more rice will be purchased, as there is not enough income left over to some consumers to purchase higher value food items.

If we then relax the assumption that other variables (such as income and tax rates, etc) are constant, what happens then? An increase in income will often cause the demand for a good or service to increase, and this will shift the whole curve away from the origin. Likewise, a reduction in the price of a substitute good will move the demand curve towards the origin as the good in question will then be less attractive to the consumer.

While these generalisations are useful, it is important to remember that economic behaviour is based on human decisions, and so we can never predict fully how people will act. For example, some very basic foodstuffs will become less popular as incomes increase and when consumers find that they no longer have to subsist on basic diets.

SUPPLY

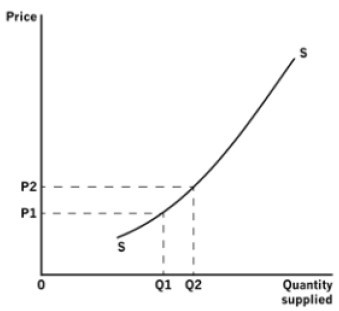

Supply refers to the quantity of goods and services offered to the market by producers. Just as we can map the relationship between quantity demanded and price, we can also consider the relationship between quantity supplied and price. Generally, suppliers will be prepared to produce more goods and services the higher the price they can obtain. Therefore, the supply curve – when holding other influences constant – will slope upwards from left to right, as illustrated in Figure 2.

Figure 2: Supply curve

There is a direct relationship between price and quantity supplied. An increase in price from OP1 to OP2 results in an increase in quantity supplied from OQ1 to OQ2.

The determinants of supply are:

· price

· prices of other goods and services

· relative revenues and costs of making the good or service

· the objectives of producers and their future expectations

· technology.

Generally, a firm will maximise profit when its marginal revenue (the revenue arising from selling one extra unit of production) equals its marginal cost (the cost of producing that one extra unit of production). However, a firm may continue to produce as long as the marginal revenue exceeds its average variable costs, as in doing so it will be making a contribution towards covering its fixed costs.

Following the same rationale as applied earlier, a movement along the supply curve will be brought about by a change in price, but a movement of the whole curve will be caused by a determinant other than price.

Page: 12 The oroginal article>>

Copyright © 2000 - www.chinaacc.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

套餐D大额券

¥

去使用

新用户扫码下载

新用户扫码下载